Optimization

Using programming languages to solve optimization problems

April 9, 2025

Lecture Summary

- Optimization

- Analytic

- Programmatic

- Symbolic

- Numeric

- Grid Search

- Gradient-free

- Gradient-based

- Automatic Differentiation

Quantecon

https://quantecon.org/lectures/

A super useful resource for learning about quantitative methods for solving economic models.

most lectures using Python, some using Julia

macro / finance focus

also a package of useful functions for Python and Julia

Optimization

Common Classes of Optimization Problems

Linear Programming (LP)

Quadratic Programing (QP)

Non-linear Programming (NLP)

There are efficient numerical methods for LP and some QP problems.

NLP problems are much harder.

R Packages for Each Class

- LP:

lpSolve - QP:

quadprog - NLP:

nloptr

We will be using nloptr today.

Numerical Optimization

Basic Macro Example

Let’s take a three equation macro model (with no stochastic shocks and no expectations). The Central Bank wants to minimize the loss function:

\[ i_t = \min_{i_t} \left( \pi_t - \pi^* \right)^2 \\ \pi_t = \kappa y_t \\ y_t = \chi i_t \]

Substituting in the Phillips curve and the IS curve, we have:

\[ i_t = \min_{i_t} \left( \kappa \chi i_t - \pi^* \right)^2 \]

Basic Macro Example

We know the FOC:

\[ \frac{\partial \mathbb{L}}{\partial i_t} = 0 = 2 \kappa \chi \left( \kappa \chi i_t - \pi^* \right) \\ i^* = \frac{1}{\kappa \chi} \pi^* \]

Which we can use to find the optimal interst rate for given values of \(\kappa\), \(\chi\), and \(\pi^*\).

If \(\kappa = 0.5\), \(\chi = 0.5\), and \(\pi^* = 2\), then: \[ i^* = \frac{1}{0.5 \cdot 0.5} \cdot 2 = 8 \]

Numerical Methods

This is a basic square-loss problem, but what if we could not use analytic methods?

Let’s look at some numerical methods that are available.

- Grid Search

- Gradient-free methods

- Gradient-based methods

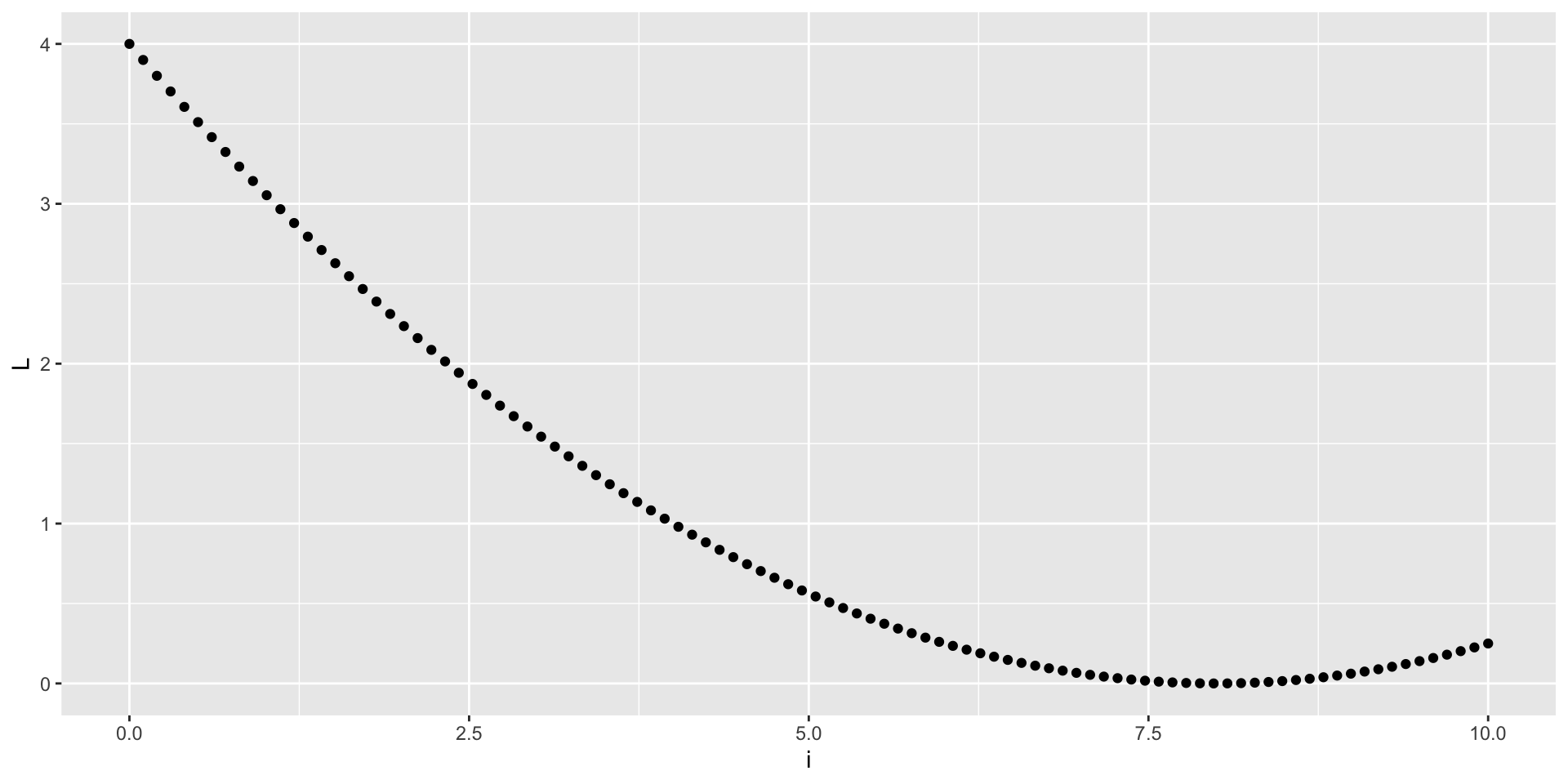

Grid Search

A grid search is a brute force method of searching for the optimal solution.

- Define a grid of values for the variable of interest (in this case, \(i_t\))

- Evaluate the loss function at each point in the grid

- Find the point with the minimum value of the loss function

- This is a very simple method, but it can be computationally expensive for large grids

Grid Search

Grid Search

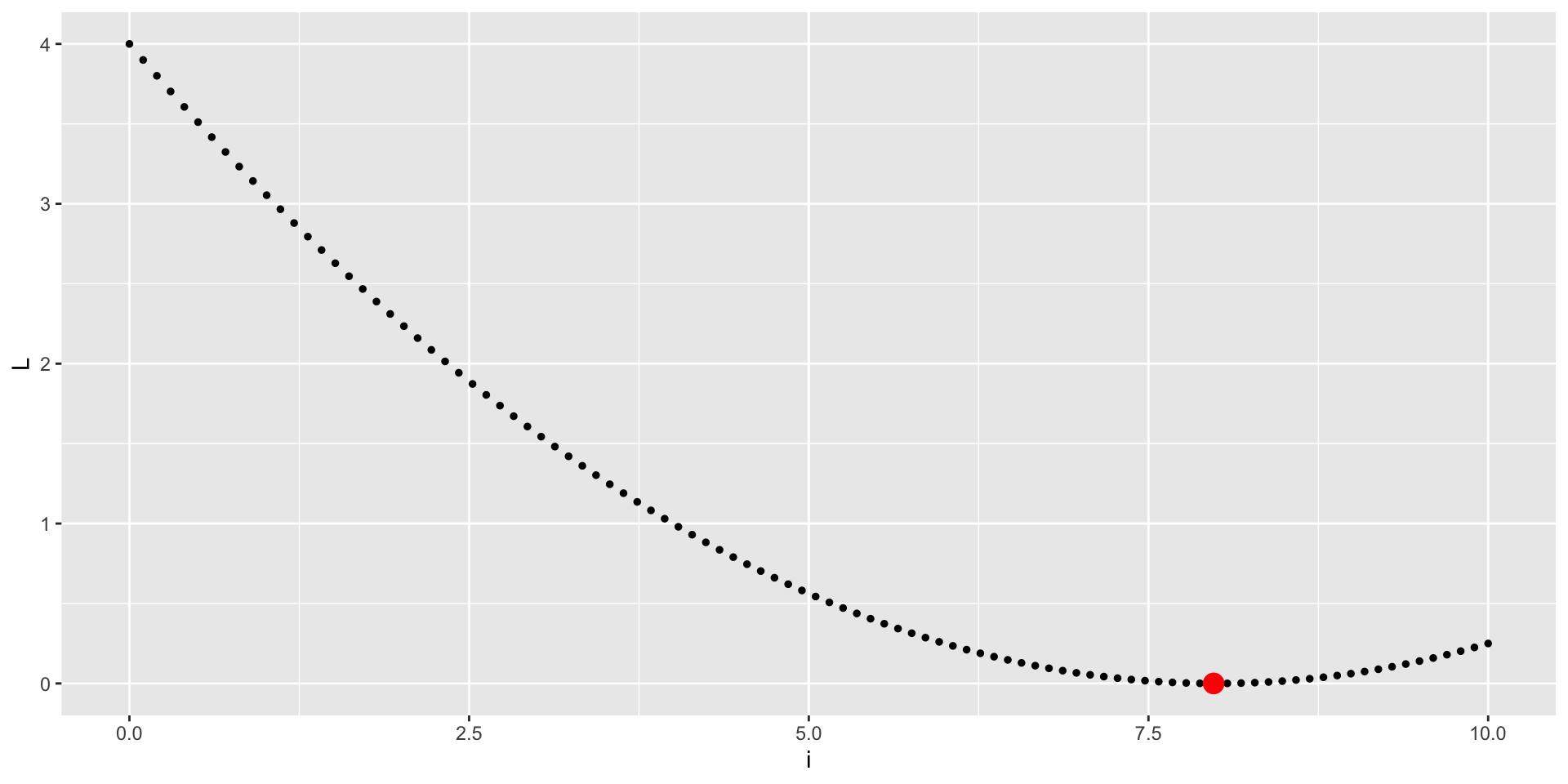

Gradient-free Methods

Gradient-free methods are useful when the loss function is not differentiable or when the gradient is difficult to compute.

One possible method is the Nelder-Mead method, which is a simplex-based optimization algorithm.

In general, gradient-free methods are less efficient than gradient-based methods.

Nonlinear Optimization in R: nloptr

nloptr is a package for nonlinear optimization and implements multiple methods.

Nelder-Mead Algorithm

The Nelder-Mead algorithm is a simplex-based optimization algorithm.

- Construct a simplex of n+1 points in n-dimensional space

- Evaluate the loss function at each point in the simplex

- Reflect, expand, or contract the simplex based on the function values

- Iterate until convergence

Nelder-Mead Method

Gradient-based Methods

Gradient-based methods are more efficient than gradient-free methods, but they require the loss function to be differentiable.

One of the simplest gradient methods is Newton’s Method for optimization.

Newton’s Method for Optimization

Optimizes a function \(f(x)\) by finding roots for \(f^\prime(x)=0\).

- Start with an initial guess \(x_0\)

- Compute the gradient \(f^\prime(x_0)\)

- Compute the Hessian \(f^{\prime\prime}(x_0)\)

- Update the guess \(x_1 = x_0 - \frac{f\prime(x_0)}{f\prime\prime(x_0)}\)

- Repeat until convergence

Some Restriction of Newton’s Method

- Requires kndowledge of the gradient

- Requires the Hessian to exist and be invertible

Quasi-Newton methods are a class of methods that approximate the Hessian.

- BFGS is a popular quasi-Newton method that approximates the Hessian with changes in the gradient

- Truncated Newton Method also approximates the Hessian

Truncated Newton’s Method

Numerical Gradient

Instead of computing the gradient analytically, we can use a numerical approximation.

This approximates the gradient using finite differences.

\[ f^\prime(x) \approx \frac{f(x + h) - f(x - h)}{2h} \]

where \(h\) is small.

Truncated Newton’s Method, numerical gradient

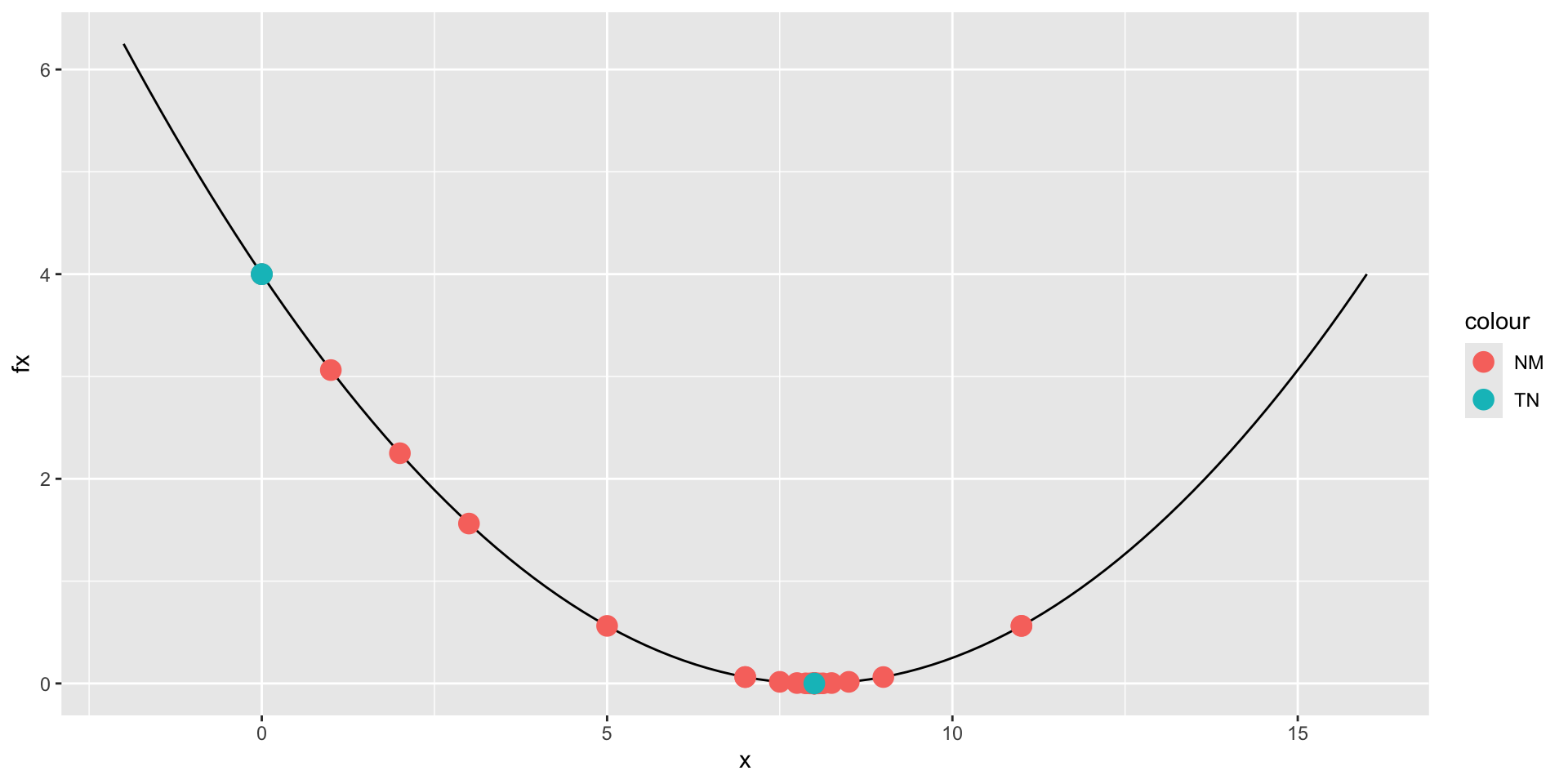

Tracking the Iterations

It can be confusing to understand what is happening in the optimization process.

We can tell nloptr to save the intermediate values of the optimization process.

opts <- list(

"algorithm" = "NLOPT_LN_NELDERMEAD",

"xtol_rel" = 0.0001,

"maxeval" = 100,

"print_level" = 3

)

nloptr(x0 = 0, eval_f = L, opts = opts)iteration: 1

x = 0.000000

f(x) = 4.000000

iteration: 2

x = 1.000000

f(x) = 3.062500

iteration: 3

x = 2.000000

f(x) = 2.250000

iteration: 4

x = 3.000000

f(x) = 1.562500

iteration: 5

x = 5.000000

f(x) = 0.562500

iteration: 6

x = 7.000000

f(x) = 0.062500

iteration: 7

x = 11.000000

f(x) = 0.562500

iteration: 8

x = 9.000000

f(x) = 0.062500

iteration: 9

x = 11.000000

f(x) = 0.562500

iteration: 10

x = 8.000000

f(x) = 0.000000

iteration: 11

x = 7.000000

f(x) = 0.062500

iteration: 12

x = 8.500000

f(x) = 0.015625

iteration: 13

x = 7.500000

f(x) = 0.015625

iteration: 14

x = 8.250000

f(x) = 0.003906

iteration: 15

x = 7.750000

f(x) = 0.003906

iteration: 16

x = 8.125000

f(x) = 0.000977

iteration: 17

x = 7.875000

f(x) = 0.000977

iteration: 18

x = 8.062500

f(x) = 0.000244

iteration: 19

x = 7.937500

f(x) = 0.000244

iteration: 20

x = 8.031250

f(x) = 0.000061

iteration: 21

x = 7.968750

f(x) = 0.000061

iteration: 22

x = 8.015625

f(x) = 0.000015

iteration: 23

x = 7.984375

f(x) = 0.000015

iteration: 24

x = 8.007812

f(x) = 0.000004

iteration: 25

x = 7.992188

f(x) = 0.000004

iteration: 26

x = 8.003906

f(x) = 0.000001

iteration: 27

x = 7.996094

f(x) = 0.000001

iteration: 28

x = 8.001953

f(x) = 0.000000

iteration: 29

x = 7.998047

f(x) = 0.000000

iteration: 30

x = 8.000977

f(x) = 0.000000

iteration: 31

x = 7.999023

f(x) = 0.000000

iteration: 32

x = 8.000488

f(x) = 0.000000

Call:

nloptr(x0 = 0, eval_f = L, opts = opts)

Minimization using NLopt version 2.10.0

NLopt solver status: 4 ( NLOPT_XTOL_REACHED: Optimization stopped because

xtol_rel or xtol_abs (above) was reached. )

Number of Iterations....: 32

Termination conditions: xtol_rel: 1e-04 maxeval: 100

Number of inequality constraints: 0

Number of equality constraints: 0

Optimal value of objective function: 0

Optimal value of controls: 8Tracking the Iterations

nloptr does not return these intermediate values, but we can write some custom functions to capture them and clean them into a data.frame.

parse_optim_output <- function(text) {

# Initialize vectors to store data

iteration <- numeric()

x <- numeric()

fx <- numeric()

# Process each group of 3 lines

for(i in seq(1, length(text), 3)) {

# Extract iteration number

iter <- as.numeric(gsub("iteration: ", "", text[i]))

# Extract x value using regex

x_val <- as.numeric(gsub("\\s*\\tx = ", "", text[i+1]))

# Extract function value

f_val <- as.numeric(gsub("\\s*f\\(x\\) = ", "", text[i+2]))

# Append values

iteration <- c(iteration, iter)

x <- c(x, x_val)

fx <- c(fx, f_val)

}

# Create data.frame

data.frame(

iteration = iteration,

x = x,

fx = fx

)

}

my_nloptr <- function(...){

m <- capture.output({

o <- nloptr(...)

})

df_m <- parse_optim_output(m)

return(list(opt = o, iter = df_m))

}Tracking the Iterations

opts <- list(

"algorithm" = "NLOPT_LN_NELDERMEAD",

"xtol_rel" = 0.0001,

"maxeval" = 100,

"print_level" = 3

)

o <- my_nloptr(x0 = 0, eval_f = L, eval_grad_f = dL, opts = opts)

o$iter iteration x fx

1 1 0.000000 4.000000

2 2 1.000000 3.062500

3 3 2.000000 2.250000

4 4 3.000000 1.562500

5 5 5.000000 0.562500

6 6 7.000000 0.062500

7 7 11.000000 0.562500

8 8 9.000000 0.062500

9 9 11.000000 0.562500

10 10 8.000000 0.000000

11 11 7.000000 0.062500

12 12 8.500000 0.015625

13 13 7.500000 0.015625

14 14 8.250000 0.003906

15 15 7.750000 0.003906

16 16 8.125000 0.000977

17 17 7.875000 0.000977

18 18 8.062500 0.000244

19 19 7.937500 0.000244

20 20 8.031250 0.000061

21 21 7.968750 0.000061

22 22 8.015625 0.000015

23 23 7.984375 0.000015

24 24 8.007812 0.000004

25 25 7.992188 0.000004

26 26 8.003906 0.000001

27 27 7.996094 0.000001

28 28 8.001953 0.000000

29 29 7.998047 0.000000

30 30 8.000977 0.000000

31 31 7.999023 0.000000

32 32 8.000488 0.000000Visualizing the Iterations

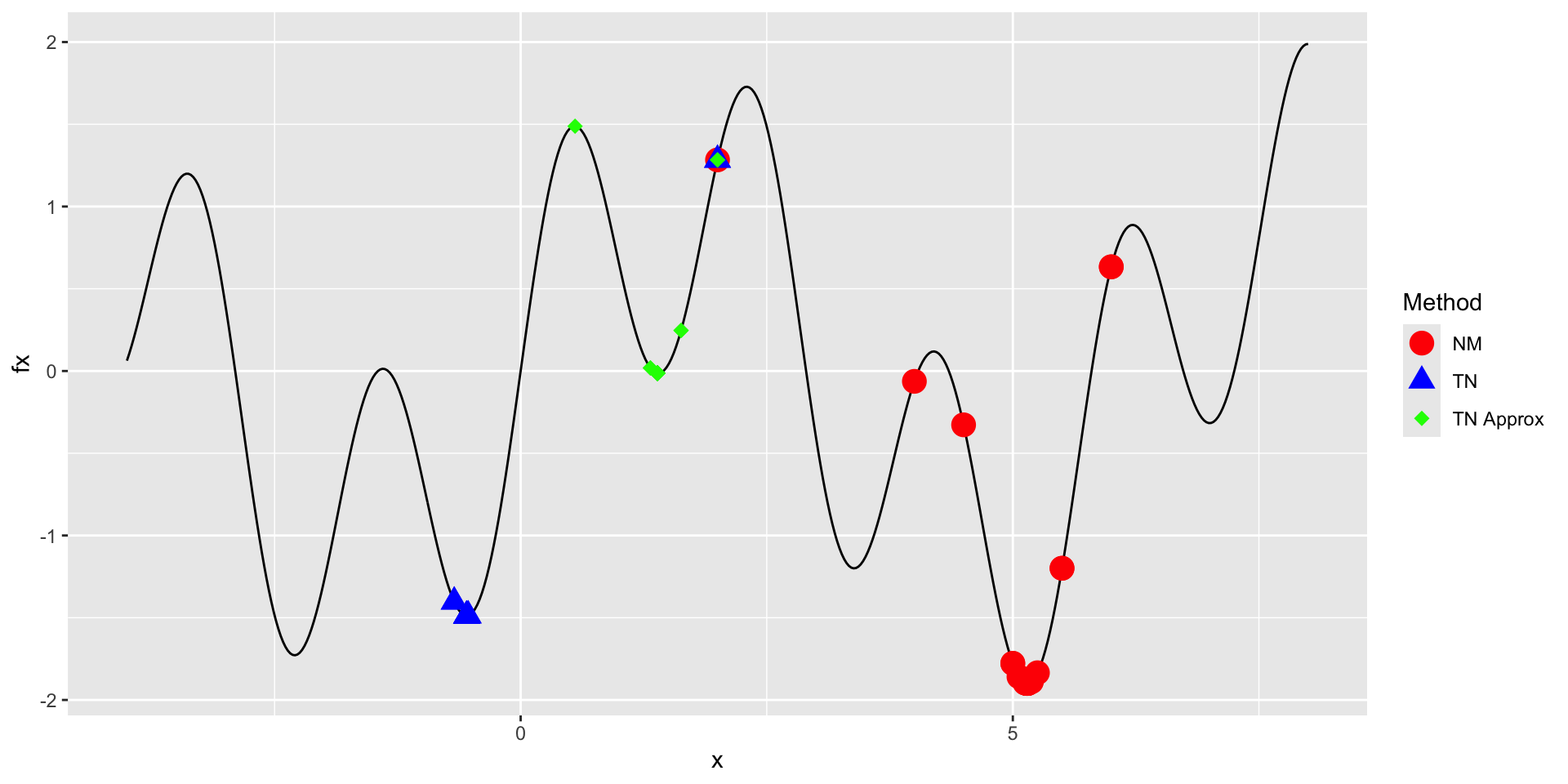

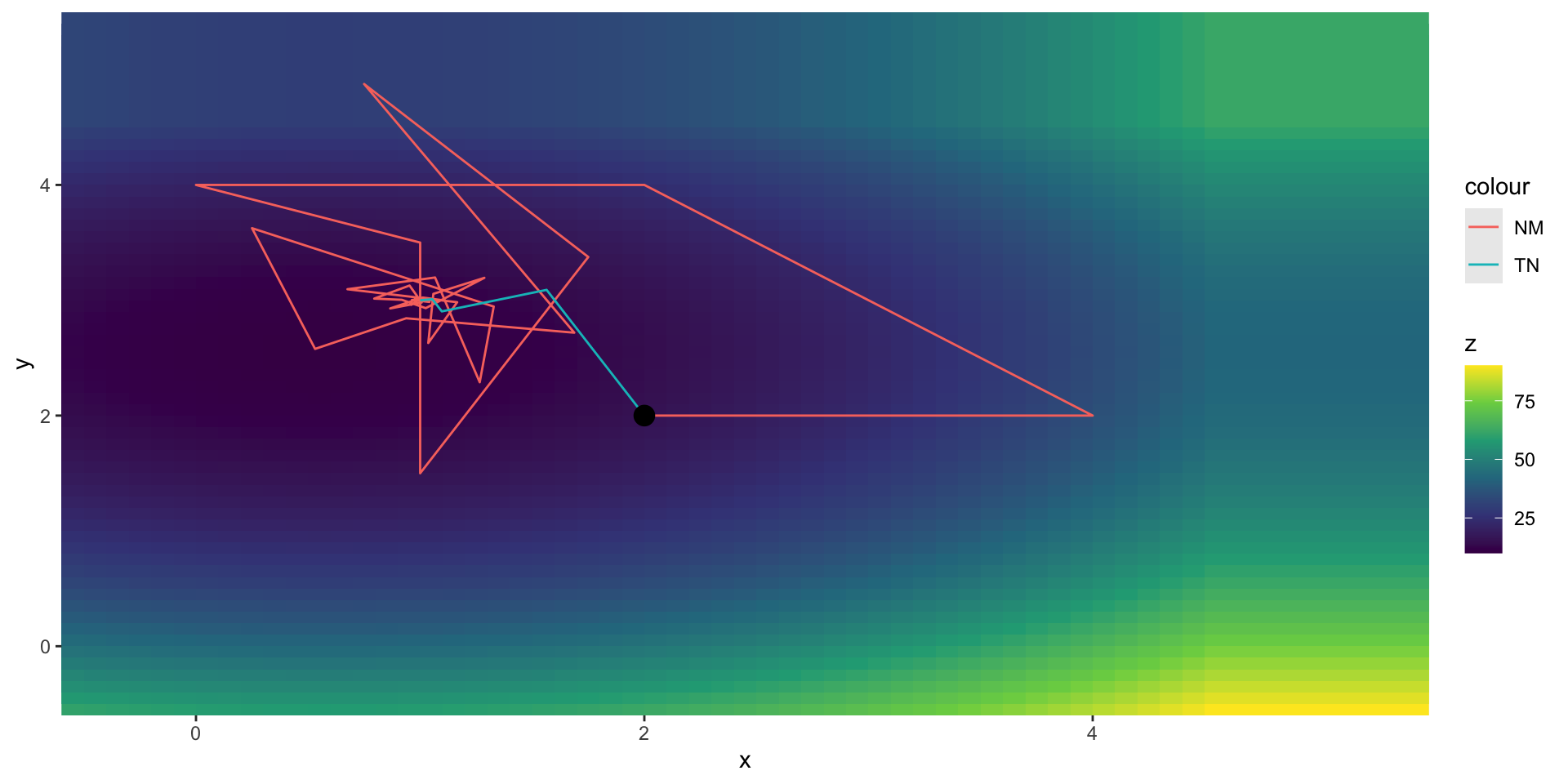

Comparing Methods

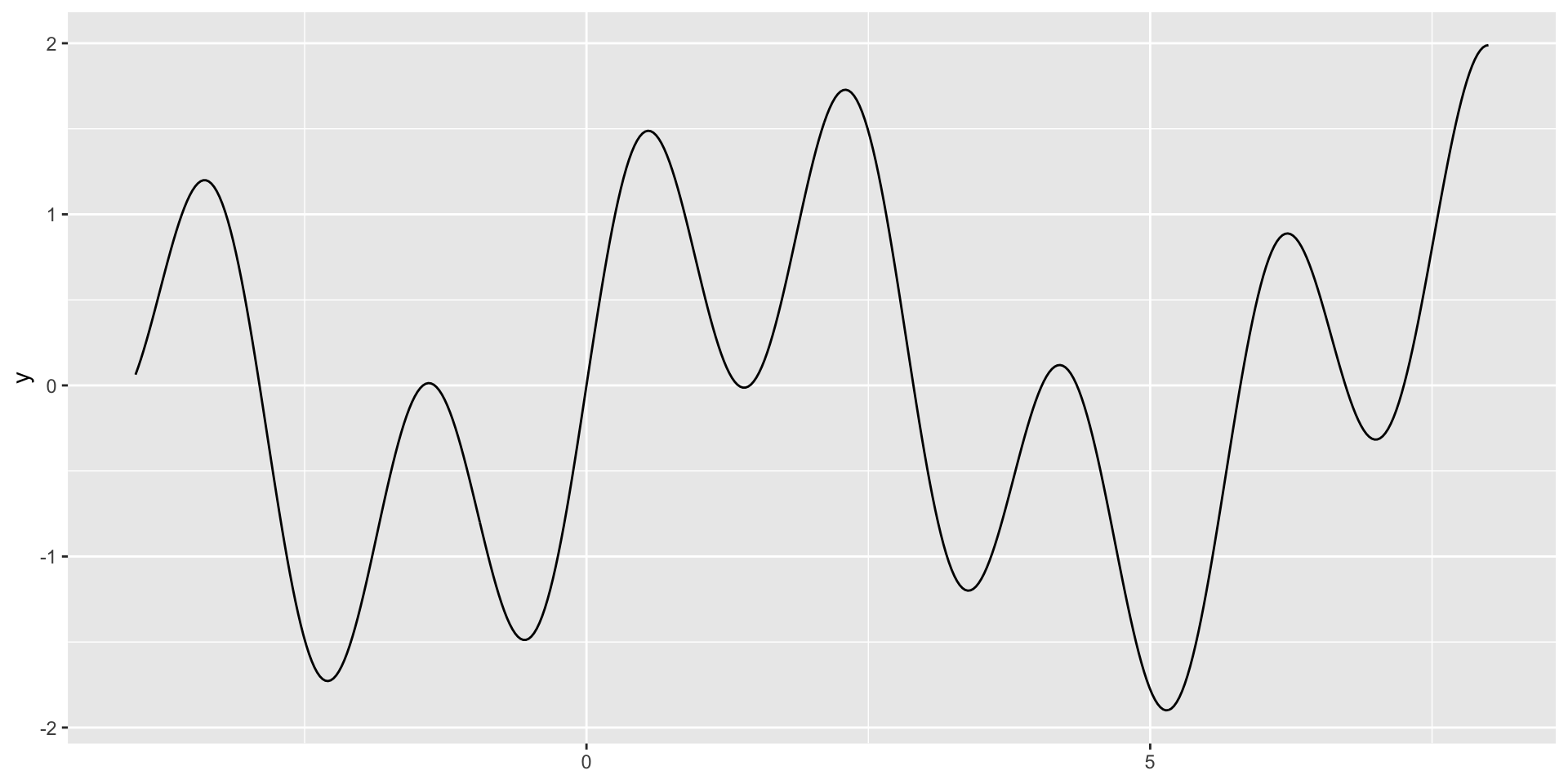

Local Minima

Let’s look at a more complicated example.

Numerical Approximation of Gradient

Again, we can use a numerical approximation of the gradient.

The argument heps is the step size for the numerical approximation.

- setting

hepsto a large value to show the difference between using the numerical and analytical gradient

Calculating Minima

opts <- list(

"algorithm" = "NLOPT_LN_NELDERMEAD",

"xtol_rel" = 0.0001,

"maxeval" = 100,

"print_level" = 3

)

o_nm <- my_nloptr(x0 = 2, eval_f = f, opts = opts)

opts <- list(

"algorithm" = "NLOPT_LD_TNEWTON",

"xtol_rel" = 0.0001,

"maxeval" = 100,

"print_level" = 3

)

o_tn <- my_nloptr(x0 = 2, eval_f = f, eval_grad_f = d, opts = opts)

opts <- list(

"algorithm" = "NLOPT_LD_TNEWTON",

"xtol_rel" = 0.0001,

"maxeval" = 100,

"print_level" = 3

)

o_tn_approx <- my_nloptr(x0 = 2, eval_f = f, eval_grad_f = d_approx, opts = opts)Comparing Methods

Comparing Methods

Solutions:

[[1]]

[1] 5.145508

[[2]]

[1] -0.5488825

[[3]]

[1] 1.389585Number of iterations:

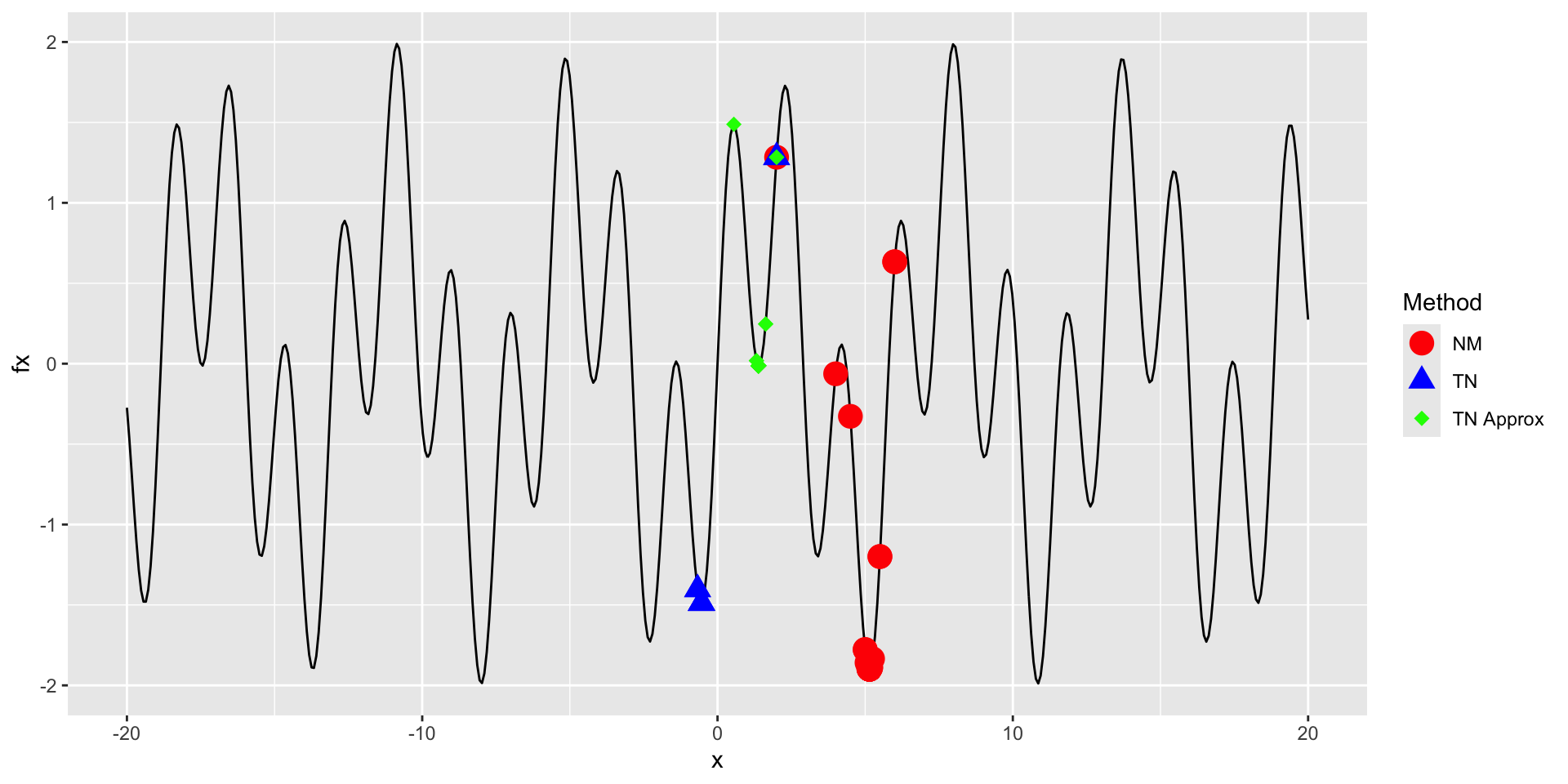

Zooming Out

All methods are finding local minima as this function is difficult to optimize.

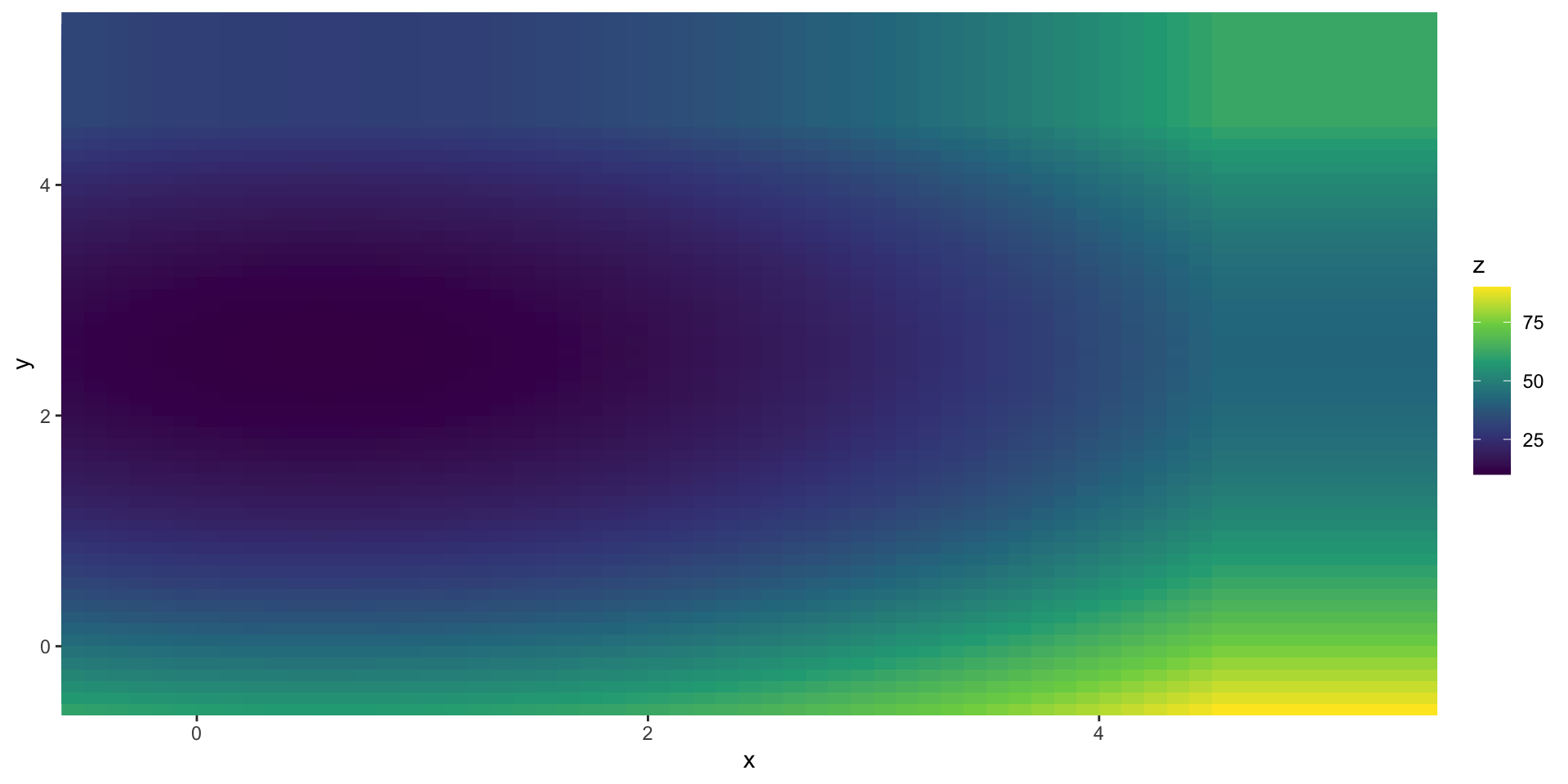

Optimizing Over Multiple Arguments

So far we have been optimizing over a single variable.

But we can optimize over as many variables as we want.

Graph the Function

Optimizing Over Multiple Arguments

opts <- list(

"algorithm" = "NLOPT_LD_TNEWTON",

"xtol_rel" = 0.0001,

"maxeval" = 100

)

nloptr(x0 = c(2, 2), eval_f = f, eval_grad_f = d, opts = opts)

Call:

nloptr(x0 = c(2, 2), eval_f = f, eval_grad_f = d, opts = opts)

Minimization using NLopt version 2.10.0

NLopt solver status: 1 ( NLOPT_SUCCESS: Generic success return value. )

Number of Iterations....: 10

Termination conditions: xtol_rel: 1e-04 maxeval: 100

Number of inequality constraints: 0

Number of equality constraints: 0

Optimal value of objective function: 10

Optimal value of controls: 1 3Visualizing the Iterations

Comparing the Methods

Numerical Optimization Overview

- Grid Search

- Brute force, inefficient, good at global optima

- Gradient-free methods

- less efficient, good for non-differentiable functions

- Gradient-based methods

- more efficient, requires an analytic or numeric gradient

Solving Optimization Problems

Generally, you try to solve an optimization problem by…

Finding an analytic solution by hand

Finding an analytic solution with a Symbolic engine

Numerical optimization

- gradient-based method

- grid search

When turning to numerical optimization, the key is finding or approximating the gradient.

- automatic differentiation (AD) is another method for calculating the gradient of a function

Symbolic Optimization

What is Symbolic Optimization?

When you solve an optimization problem by hand, you apply a set of rules to find the gradient, then rearrange the FOC to find zero roots.

A symbolic engine emulates this same process.

- Mathematica is an example of a common symbolic engine

Python has a great symbolic engine called SymPy which we will take a look at.

Automatic Differentiation

What is Automatic Differentiation?

We have so far seen two ways to calculate the gradient of a function:

- Analytically (or symbollically)

- Finite differences (approximation up to some order ‘n’)

- Automatic differentiation (AD)

- a method for calculating the derivative of a function using the chain rule

AD Chain Rule

\[ \begin{align*} y &= f(g(h(x))) = f(g(h(w_0))) = f(g(w_1)) = f(w_2) \\ w_0 &= x \\ w_1 &= h(w_0) \\ w_2 &= g(w_1) \\ w_3 &= f(w_2) = y \\ \frac{dy}{dx} &= \frac{dy}{dw_2} \cdot \frac{dw_2}{dw_1} \cdot \frac{dw_1}{dx} \\ &= \frac{df(w_2)}{dw_2} \cdot \frac{dg(w_1)}{dw_1} \cdot \frac{dh(w_0)}{dw_0} \end{align*} \]

The “trick” of AD is that we can build up complicated composite functions as a series of partial derivatives of each step.

Forward vs. Reverse Mode AD

\[ \frac{dy}{dx} = \frac{dy}{dw_2} \cdot \frac{dw_2}{dw_1} \cdot \frac{dw_1}{dx} \]

Forward AD calculates:

- \(\frac{dw_1}{dx}\) then \(\frac{dw_2}{dw_1}\) then \(\frac{dy}{dw_2}\)

Reverse AD calculates:

- \(\frac{dy}{dw_2}\) then \(\frac{dw_2}{dw_1}\) then \(\frac{dw_1}{dx}\)

Forward vs. Reverse Mode AD

Given a function \(f: \mathbb{R}^n \to \mathbb{R}^m\)

- if \(n << m\), then forward mode is more efficient

- if \(n >> m\), then reverse mode is more efficient

For a loss function, \(f: \mathbb{R}^n \to \mathbb{R}\), so reverse mode is more efficient.

A Simple AD example

\[ \begin{align*} f(x_1, x_2) &= x_1 x_2 + sin(x_1) \\ &= w_1 + w_2 \\ &= w_3 \\ \frac{dy}{dx} &= \frac{dw_3}{dw_1} \cdot \frac{dw_1}{dx} + \frac{dw_3}{dw_2} \cdot \frac{dw_2}{dx} \end{align*} \]

In this example, each step is easy to calculate:

\[ \frac{dy}{dx} = \underbrace{\frac{dw_3}{dw_1}}_{1} \cdot \underbrace{\frac{dw_1}{dx}}_{x_1 + x_2} + \underbrace{\frac{dw_3}{dw_2}}_{1} \cdot \underbrace{\frac{dw_2}{dx}}_{cos(x_1)} \]

Because this problem was simple, when we follow the AD chain rule, we derive the symbolic solution.

AD vs. Symbolic Differentiation

AD, however, can be used in many cases where symbolic differentiation is not possible.

Automatic Differentiation is usually calculated only for a single point at a time, not for the entire function.

This means it can handle functions that

- are not differentiable everywhere

- cannot be “written down”

- are not continuous

AD does require that a function can be written programmatically/algorithmically.

AD in Machine Learning

Automatic Differeneiation is the key step behind fitting large neural networks.

Neural networks have the following features/goals:

- A loss function with many paramaeters: \(f: \mathbb{R}^n \to \mathbb{R}\)

- Can be written programmatically, but not symbolically

- Cares about precision and efficiency

- But doesn’t care about a closed-form expression of the gradient

More AD Resources

- What’s Automatic Differentiation? by Andrew Holmes

- Automatic Differentation Wikipedia

- Automatic Differentation JAX Python Documentation

Summary

Lecture Summary

- Optimization

- Analytic

- Programmatic

- Symbolic

- Numeric

- Grid Search

- Gradient-free

- Gradient-based

- Automatic Differentiation

Live Coding Example

Python

SympyCoding Example (symoblic)Python

JAXCoding Example (automatic differentiation)